Running a Seattle business means navigating B&O tax on gross receipts, state sales tax requirements, and some of the highest payroll costs in the country. Most owners work hard inside their business — fewer consistently step back to review the numbers that guide it.

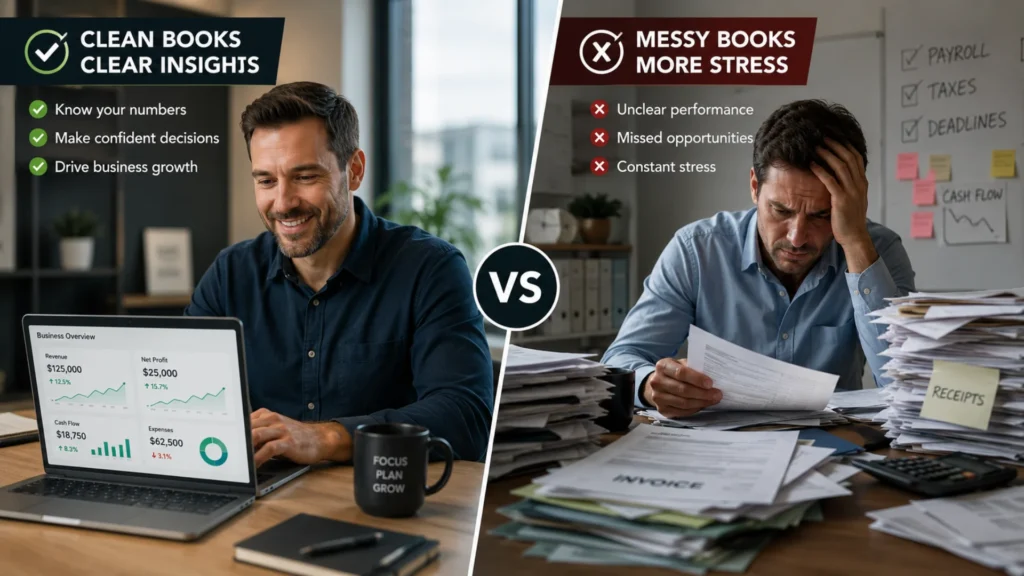

Monthly financial review is not just an accounting exercise. It is a leadership discipline. Businesses that review the right reports monthly operate with clarity. Businesses that do not operate reactively.

This guide outlines the 10 financial reports every Seattle business owner should review each month — and why each one matters.

Why Monthly Financial Review Matters for Seattle Businesses

Seattle businesses face a unique combination of cost pressures:

- B&O tax applied to gross revenue

- Sales tax collection requirements

- High payroll costs

- Competitive vendor markets

- Rapid startup growth cycles

- Seasonal revenue variability

Without consistent monthly review, tax liabilities become unclear, cash flow surprises emerge, margin compression goes unnoticed, and CPA cleanup fees increase. Monthly reporting creates predictability — and predictability creates control.

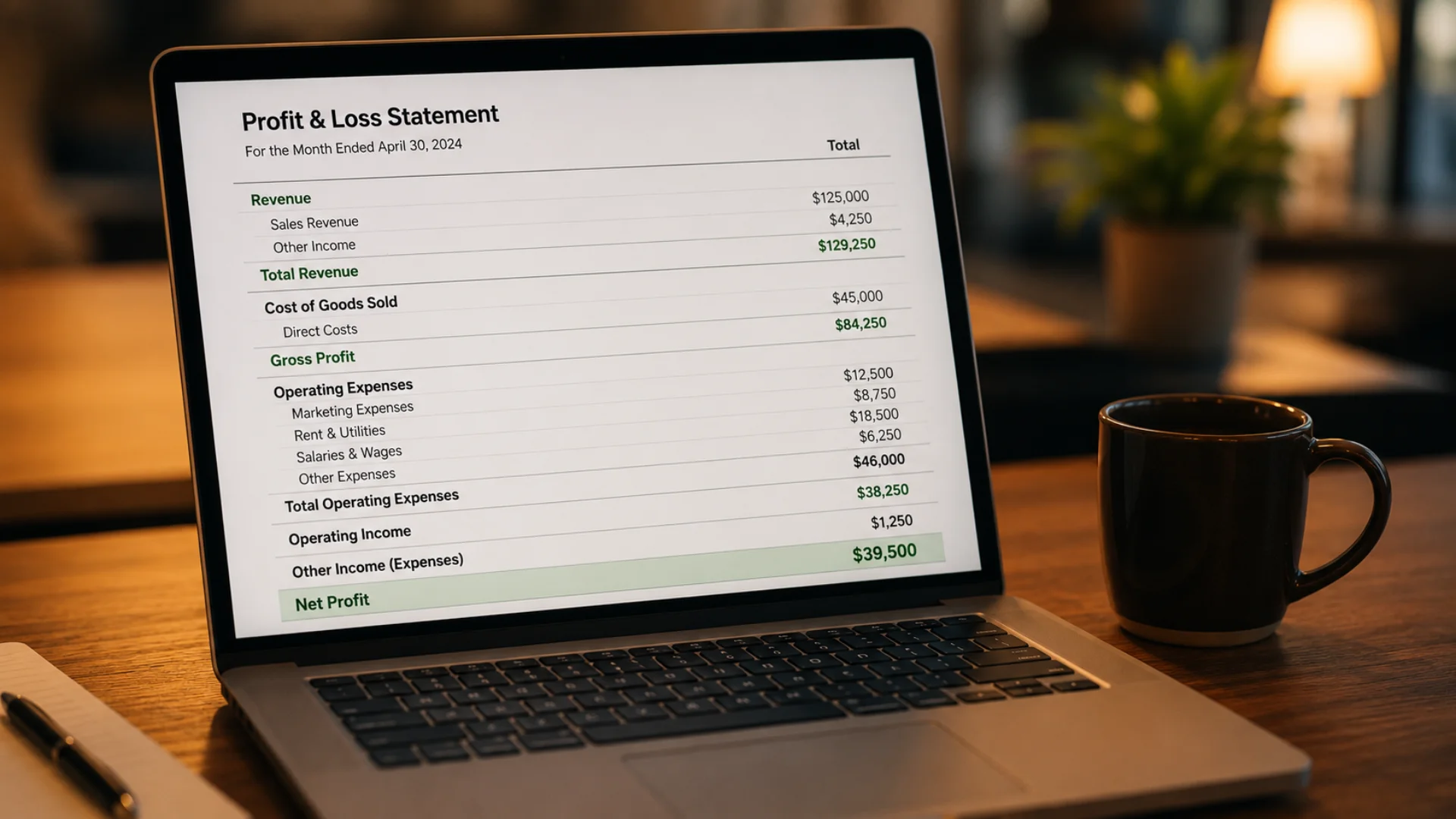

1. Profit & Loss Statement (Income Statement)

The Profit & Loss (P&L) statement summarizes revenue, cost of goods sold, gross profit, operating expenses, and net profit. It answers the core question: Is the business profitable this month?

What Seattle owners should look for:

Revenue Trends: Is revenue increasing, flat, or declining compared to prior months? For Washington businesses, revenue tracking also directly impacts B&O liability.

Gross Margin: If you sell products or manage food costs — restaurants, contractors, retail — gross margin should be reviewed monthly. Small shifts in cost percentage can significantly impact profit.

Operating Expenses: Watch for vendor cost creep, rising software subscriptions, marketing spend increases, and payroll growth. Trend analysis prevents expense drift.

Net Profit: Net profit indicates sustainability. However, profitability alone does not guarantee cash flow strength — which is why the reports below matter just as much.

2. Balance Sheet

The Balance Sheet shows assets, liabilities, and equity. It answers: What does the business own, and what does it owe?

Key areas to review:

Cash: Does the reported cash match reconciled bank accounts? If accounts are not reconciled monthly, this number may be inaccurate.

Accounts Receivable: Are customers paying on time? High receivables can create cash flow strain even when revenue looks strong.

Accounts Payable: Are vendor obligations growing faster than revenue? Unmonitored payables can indicate cash pressure.

Sales Tax Payable: Is the liability consistent with collected tax? Collected tax is not revenue — it must be monitored carefully.

B&O Accrual: Washington B&O applies to gross receipts. Monthly accrual ensures predictability and prevents filing surprises.

Loans & Lines of Credit: Is debt increasing? Is it manageable relative to revenue? The Balance Sheet reveals long-term stability.

3. Cash Flow Statement

The Cash Flow Statement tracks cash inflows, cash outflows, operating cash flow, investing activities, and financing activities. It answers: Why did cash increase or decrease this month?

Profit and cash are not the same thing. Seattle businesses often experience cash strain due to payroll timing, tax payments, equipment purchases, and vendor terms. Cash flow analysis clarifies liquidity when the P&L alone cannot.

4. Revenue Detail Report

This report breaks down revenue by category — and for Seattle businesses with multiple revenue streams, it is critical. Examples include service vs. product revenue, dine-in vs. delivery, subscription vs. project billing, and taxable vs. non-taxable revenue.

Revenue segmentation helps identify high-margin services, underperforming offerings, and pricing opportunities. Strategic growth depends on this kind of clarity.

5. Expense Detail Report

Beyond summary categories, reviewing detailed expenses helps identify duplicate charges, subscription accumulation, vendor pricing increases, and unusual transactions. Monthly detail review prevents small leaks from becoming large losses.

6. Payroll Summary Report

Seattle’s wage environment makes payroll monitoring essential. Review total payroll expense, payroll taxes, overtime, and labor percentage of revenue each month. For most businesses, payroll is the largest expense category — and monitoring the labor percentage monthly directly protects margins.

7. Sales Tax Liability Report

For businesses collecting sales tax, monthly review should confirm taxable sales, non-taxable sales, collected tax totals, and liability balances. Confirm that liability matches collected amounts, tax is segregated properly, and filing amounts align with bookkeeping records. Sales tax clarity prevents compliance issues and the cash surprises that come with them.

8. B&O Tracking Summary

Washington businesses must monitor B&O liability every month — not just at filing time. Review gross revenue totals, applicable tax classifications, accrued tax balance, and filing schedule. B&O surprises create cash strain. Monthly tracking eliminates that uncertainty entirely.

9. Accounts Receivable Aging Report

This report shows how long invoices remain unpaid: current, 30-day, 60-day, and 90+ day balances. Delayed payments reduce liquidity even when the P&L looks healthy. Monitoring AR supports proactive collections and protects cash flow.

10. Accounts Payable Aging Report

This report shows vendor obligations, payment timing, and cash commitments. Reviewing payables ensures vendor relationships remain strong, cash flow is aligned with obligations, and no payments are missed. Structure builds reliability.

How Long Should Monthly Financial Review Take?

With clean books, 30–60 minutes per month is typically sufficient. The key is consistency. Monthly cadence builds financial awareness faster than any other habit.

What Happens When Owners Skip Monthly Review

Businesses that review financials only quarterly or annually often experience tax surprises, margin confusion, cash flow strain, increased CPA cleanup costs, and stress during filing season. These are preventable outcomes — not inevitable ones.

Reports vs. Insight: What Makes the Difference

Reports provide numbers. Insight requires reconciliation discipline, proper categorization, tax accrual tracking, and human oversight. Automation can generate reports. Accountability ensures they are reliable.

If your books are not reconciled monthly, the reports they produce may look complete — but they are not accurate. That distinction matters enormously for the decisions you make from them.

Signs You May Not Be Reviewing the Right Reports

- You rely primarily on your bank balance

- Tax liabilities feel unclear heading into each quarter

- Your CPA frequently makes adjustments

- Revenue streams are not segmented

- Labor percentage is unknown

- Cash flow feels reactive rather than planned

These are visibility gaps — and they are fixable with the right financial systems in place.

Financial Leadership Requires Visibility

You cannot lead what you cannot see clearly. The financial reports you review monthly determine hiring decisions, expansion timing, pricing adjustments, vendor negotiations, tax planning, and long-term stability.

Ready to Strengthen Your Monthly Financial Discipline?

On Par Bookkeeping LLC helps Seattle business owners build the monthly reporting systems that create clarity, protect margins, and eliminate financial surprises.

A structured review can identify reporting gaps, reconciliation inconsistencies, tax exposure, margin blind spots, and forecasting opportunities. So, Schedule Your Free Financial Review. Seattle businesses perform strongest when financial systems support leadership — not just compliance.