Personal injury law is one of the most financially complex areas of legal practice. Unlike many other law firms that bill clients hourly or collect flat fees, personal injury attorneys typically work under contingency fee agreements, meaning the firm is paid only if a case successfully resolves.

This structure can lead to large settlement payouts but unpredictable revenue cycles, making disciplined bookkeeping essential for financial stability.

Personal injury firms must track settlement funds, medical liens, litigation expenses, and client disbursements with precision. Funds often pass through client trust accounts before being distributed to multiple parties, including medical providers, expert witnesses, and the client.

Organizations such as the American Association for Justice and courts like the United States District Court frequently oversee or influence aspects of litigation and settlement procedures. Because personal injury cases often involve court filings, negotiations with insurance companies, and structured settlement agreements, financial recordkeeping must be detailed and transparent.

For personal injury attorneys practicing in large metropolitan markets such as Seattle, where litigation costs and case values can be substantial, strong bookkeeping systems provide the foundation for managing revenue, expenses, and regulatory obligations.

This guide explains how bookkeeping helps personal injury attorneys manage contingency fee income, track settlement funds, and maintain accurate financial records across complex legal cases.

Why Personal Injury Law Firms Have Complex Financial Structures

Personal injury law firms operate differently from many other legal practices because their revenue depends on the outcome of cases. Most personal injury cases involve incidents such as:

• automobile accidents

• workplace injuries

• medical malpractice

• product liability claims

• wrongful death cases

Instead of billing clients hourly throughout the case, attorneys often sign contingency agreements that entitle the firm to a percentage of the final settlement or court award.

Typical contingency arrangements may range from 30% to 40% of the total recovery, depending on the complexity of the case and whether litigation proceeds to trial. This model creates several financial dynamics:

• revenue may be delayed for months or years

• settlement funds must be distributed to multiple parties

• legal expenses are often advanced by the firm

• trust accounts must be carefully managed

Because of these factors, personal injury bookkeeping requires detailed tracking systems to ensure every dollar is accounted for properly.

How Contingency Fee Agreements Work in Personal Injury Law

Contingency fee arrangements are the cornerstone of personal injury legal services. Under a contingency agreement:

• the client pays no upfront legal fees

• the attorney receives a percentage of the settlement

• the firm may advance case-related expenses

If the case results in a settlement or judgment, the contingency fee is calculated based on the final recovery amount. For example, if a case settles for $300,000 and the attorney’s contingency percentage is 33%, the legal fee would be $99,000 before expenses and other deductions.

What Bookkeeping Must Track in Contingency Cases

Bookkeeping systems must track:

• total settlement amounts

• contingency percentages

• expenses advanced by the firm

• net recovery owed to the client

Accurate calculations ensure that legal fees are distributed correctly and transparently.

Managing Client Trust Accounts (IOLTA Compliance)

When settlement funds are received, they are typically deposited into a client trust account. Trust accounts ensure that settlement funds are held safely until they are properly distributed to all parties involved in the case.

These accounts are commonly structured as IOLTA accounts under professional guidelines supported by organizations such as the American Bar Association. Once settlement funds arrive in the trust account, the law firm must allocate the funds according to the settlement agreement. This process may involve:

• attorney contingency fees

• medical lien payments

• reimbursement of case expenses

• the client’s net recovery

Bookkeeping systems must maintain detailed ledgers showing how funds move through the trust account.

Key Trust Account Bookkeeping Tasks

Proper trust account management includes:

• recording settlement deposits

• documenting every disbursement

• maintaining client-specific balances

• reconciling trust account balances monthly

These procedures help ensure compliance with legal and ethical obligations governing client funds.

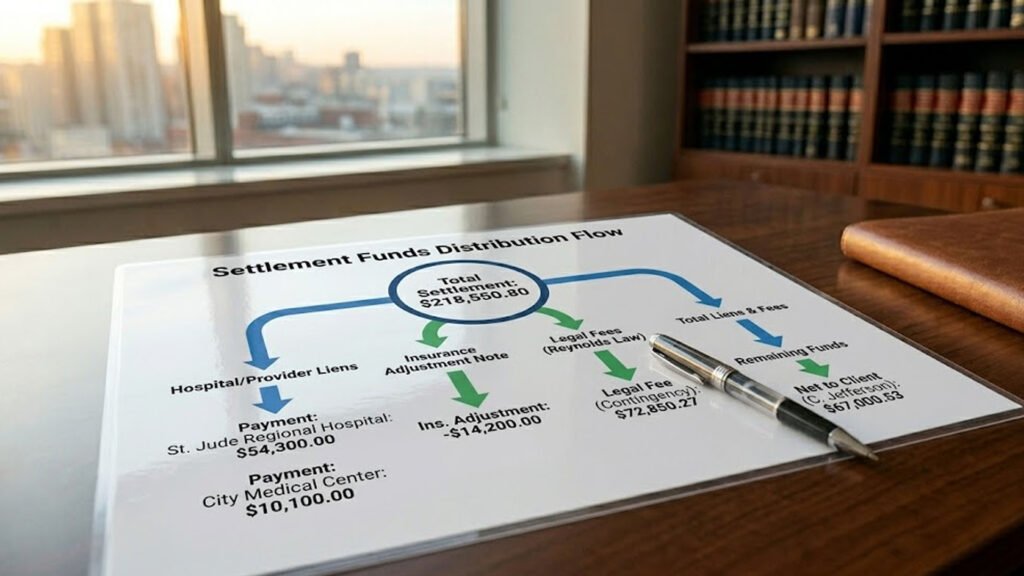

How to Track Settlement Funds Accurately

Settlement funds often pass through several stages before final distribution. A typical settlement flow may involve:

- insurance company issues settlement payment

- funds are deposited into the law firm’s trust account

- liens and expenses are calculated

- legal fees are allocated

- remaining funds are distributed to the client

Bookkeeping systems must track each step of this process. Settlement accounting records typically include:

• the gross settlement amount

• contingency fees owed to the law firm

• litigation costs advanced by the firm

• medical lien obligations

• final payment to the client

Accurate records help ensure that settlement proceeds are distributed fairly and transparently.

Managing Medical Liens in Personal Injury Cases

Medical liens are a common feature of personal injury cases. When injured clients receive medical treatment after an accident, healthcare providers may place liens on the settlement to recover the cost of care. These liens may originate from:

• hospitals

• physical therapy providers

• insurance companies

• government healthcare programs

The law firm often negotiates these liens before settlement funds are distributed. Bookkeeping systems must track:

• total lien amounts

• negotiated reductions

• payments made to medical providers

Proper lien tracking ensures that all medical obligations are satisfied before the client receives their final settlement funds.

Tracking Case Costs in Personal Injury Law

Personal injury firms frequently advance litigation expenses on behalf of clients. These costs may include:

• court filing fees

• deposition transcripts

• expert witness fees

• accident reconstruction analysis

• medical record retrieval

Some cases also involve significant investigative work or expert testimony, which can create substantial upfront expenses. Bookkeeping systems must record:

• all costs associated with each case

• whether costs are reimbursable

• the timing of reimbursements after settlement

Tracking case costs ensures that the firm recovers expenses appropriately once the case resolves.

How Case Cost Reimbursement Works After Settlement

When a case settles successfully, the law firm typically recovers the costs it advanced during litigation. The settlement accounting process usually follows this order:

- settlement funds deposited into trust

- case costs reimbursed to the law firm

- contingency fee calculated

- medical liens paid

- client receives remaining funds

Bookkeeping systems must clearly document these transactions so that financial records accurately reflect how settlement funds were distributed. Maintaining detailed settlement ledgers helps prevent disputes and ensures transparency with clients.

Managing Long Case Timelines and Delayed Revenue

Personal injury cases can take months or years to resolve. During this time, law firms may continue advancing expenses while awaiting a settlement or trial verdict.

Because revenue is delayed until the case concludes, financial planning becomes essential. Bookkeeping systems help attorneys monitor:

• outstanding case costs

• anticipated settlement values

• operating expenses for the firm

Financial reporting allows firms to maintain adequate cash reserves while waiting for cases to resolve.

How to Monitor Case Profitability in Personal Injury Law

Not all personal injury cases produce the same financial outcome. Some cases may involve minimal expenses and settle quickly, while others require extensive litigation and expert testimony. Bookkeeping systems help law firms analyze case profitability by tracking:

• total settlement value

• attorney fees earned

• expenses incurred during litigation

• time invested by the legal team

By reviewing these metrics, firms can better understand which types of cases generate the strongest financial results. This insight helps attorneys refine their case selection and pricing strategies.

Cash Flow Planning for Contingency-Based Law Firms

Because contingency fees depend on successful settlements, revenue patterns in personal injury law can be irregular. A firm may resolve several cases in one month and none the next. Structured bookkeeping allows attorneys to review financial reports that track:

• monthly operating expenses

• revenue from settled cases

• outstanding case costs

• cash reserves available for operations

Financial planning helps firms maintain stability even when case outcomes vary.

Tax Considerations for Personal Injury Law Firms

Personal injury law firms must manage various tax obligations at the federal and state level.

These obligations may include:

• federal income tax

• payroll taxes for employees

• state business taxes

In some jurisdictions, law firms are also subject to taxes based on gross revenue. For example, in Washington many professional services businesses pay the Business & Occupation tax, which applies to total revenue rather than net profit.

Accurate bookkeeping ensures that all revenue and deductible expenses are recorded properly. Well-maintained financial records simplify tax preparation and reduce the likelihood of reporting errors.

Tracking Operating Expenses in Personal Injury Firms

Beyond case-specific costs, personal injury law firms incur a variety of ongoing operating expenses. These may include:

• legal research subscriptions

• marketing and advertising campaigns

• staff salaries and benefits

• office space and administrative costs

Bookkeeping systems categorize these expenses so attorneys can review how resources are being allocated. Expense visibility helps firms maintain profitability while continuing to invest in client services.

Common Bookkeeping Mistakes Personal Injury Law Firms Make

Without organized financial systems, personal injury law firms may encounter challenges such as:

• inaccurate settlement fund tracking

• incomplete documentation of case expenses

• failure to reconcile trust accounts regularly

• improper calculation of contingency fees

• overlooking medical lien obligations

These issues can create confusion about financial performance and increase the risk of accounting errors. Consistent bookkeeping helps prevent these problems by maintaining accurate financial records.

What Proper Bookkeeping Systems Look Like for Personal Injury Firms

A well-organized bookkeeping system for a personal injury practice typically includes:

• trust account reconciliation

• settlement fund tracking

• contingency fee calculation documentation

• medical lien payment tracking

• case cost reimbursement records

• monthly financial statement preparation

These processes provide law firms with clear financial visibility and help ensure settlement funds are distributed properly.

Why Financial Organization Matters in Personal Injury Law

Personal injury attorneys help clients recover compensation after life-altering events.

Because settlements often involve large financial amounts and multiple parties, maintaining accurate financial records is essential. Structured bookkeeping provides:

• transparent settlement accounting

• reliable financial reporting

• organized trust account management

• improved cash flow planning

These benefits allow attorneys to focus on advocating for their clients while maintaining confidence in the financial health of their practice.

Need Help Managing Your Personal Injury Firm’s Finances?

Handling contingency fees, settlement funds, and case costs can quickly become overwhelming without the right system in place. Accurate bookkeeping ensures every dollar is tracked, every disbursement is clear, and your firm stays compliant.

Get professional bookkeeping support and focus on winning cases while your finances stay organized and stress-free.